Reverse Mortgage for Hearing Aids and Vision Equipment: Sensory Health in Retirement

Learn how Ontario seniors can use reverse mortgages to fund hearing aids, vision devices, and sensory health equipment to maintain independence and quality of life.

As we age, our sensory abilities often decline, but the technology to address hearing and vision loss keeps improving. For Ontario seniors on a fixed income, the cost of quality hearing aids and vision equipment can feel overwhelming. A reverse mortgage offers a practical way to fund these essential devices without disrupting your retirement budget.

This article is for educational purposes only and does not constitute financial advice.

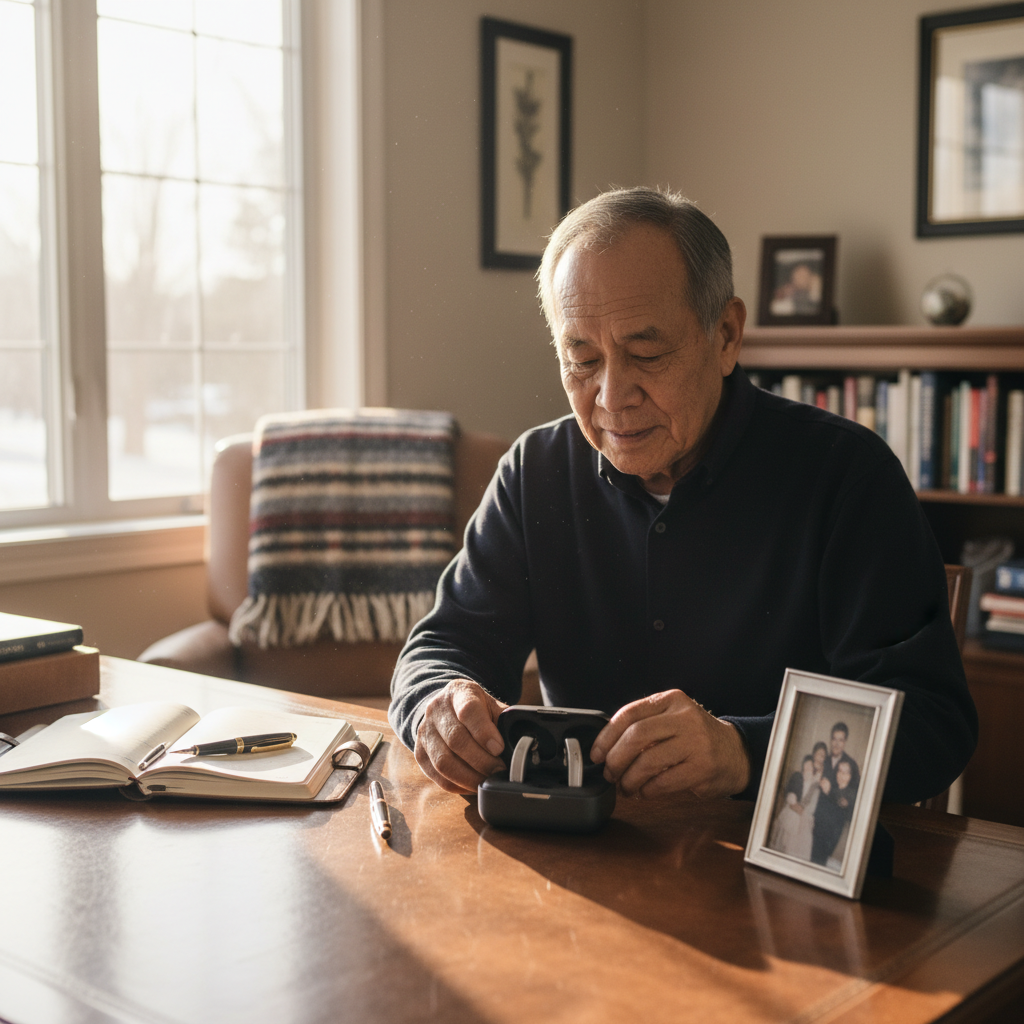

The Real Cost of Sensory Equipment

Hearing aids and vision correction devices represent significant expenses. A single hearing aid can cost between $2,000 and $6,000, and most people need two. Advanced models with wireless connectivity and noise reduction can exceed $8,000 per pair. Vision equipment—including progressive lenses, specialized glasses for macular degeneration, or devices like magnifiers—adds another layer of expense.

Many Canadians delay these purchases because they're not covered by provincial health plans. While some private insurance may help, gaps remain, leaving seniors to choose between affordability and quality of life.

Why These Devices Matter for Independence

Hearing loss and vision decline directly impact your ability to stay in your home safely and independently. Hearing aids allow you to participate in conversations, monitor for danger, and maintain social connections. Vision correction enables you to read, drive (if permitted), navigate your home, and manage daily tasks.

Delaying these purchases often leads to bigger problems: falls due to poor vision, social isolation from hearing loss, and eventually, premature moves to assisted living. Investing in sensory health equipment is an investment in aging in place.

How a Reverse Mortgage Helps

A reverse mortgage provides tax-free funds in a lump sum or through a line of credit. Unlike a traditional loan, there are no monthly payments. You continue to own your home and receive funds based on your age and home value.

For sensory equipment, a reverse mortgage is often more suitable than other borrowing options because:

- No income verification required — you don't need employment income or pension details

- Simple approval — age 55+, a home in Ontario, and clear title are the main requirements

- Flexible access — some lenders offer a line of credit for staged purchases (initial hearing aids, then follow-up equipment)

- Funds are tax-free — the money you receive is not taxable income and doesn't affect OAS or GIS

Real-World Scenario

Consider Margaret, 68, a Toronto homeowner with a $450,000 home and a fixed pension of $2,500 per month. She needs hearing aids ($5,500) and specialized glasses ($1,200) but doesn't want to dip into her emergency savings.

With a reverse mortgage, Margaret can borrow approximately $150,000–$165,000 (depending on her age and property value). She uses $6,700 for sensory equipment, maintains a line of credit for future health needs, and continues her retirement without financial stress.

What to Know Before You Borrow

Compound Interest: Reverse mortgages charge interest on the borrowed amount. If Margaret borrows $6,700 at 7.5% annually and doesn't repay it, the debt grows to approximately $7,900 after five years. This is important to understand—the longer you borrow, the larger the loan becomes.

Impact on Inheritance: The reverse mortgage debt is paid from the home's sale proceeds when you sell, move, or pass away. If you borrow $10,000 and your heirs want to keep the home, they must repay the debt plus accrued interest from other sources.

Lender Requirements: In Ontario, major reverse mortgage lenders include CHIP (HomeEquity Bank), Equitable Bank, Bloom Financial, and Home Trust. Each has slightly different terms and rates. Independent legal advice is required before closing.

No Negative Equity Guarantee: You'll never owe more than your home is worth—this is a legal guarantee in Canada's reverse mortgage market.

Timeline and Process

The reverse mortgage process typically takes 4–6 weeks:

- Initial consultation — speak with a licensed mortgage professional at Rick Sekhon Reverse Mortgages

- Property appraisal — the lender orders a home valuation (you don't pay)

- Application and approval — underwriting and final approval

- Independent legal advice (ILA) — required in Ontario; you meet with a lawyer to ensure you understand the product

- Closing — funds are released, usually via wire transfer

- Purchase — you can immediately buy your hearing aids or vision equipment

Alternatives to Consider

Before choosing a reverse mortgage, explore these options:

- Hearing aid and vision coverage programs — some charities and government programs offer subsidies for low-income seniors

- Home Equity Line of Credit (HELOC) — if you have income or employment, a HELOC may offer lower interest rates, but requires monthly payments

- Payment plans — some audiology clinics and optometrists offer financing with no interest if paid within 12 months

- Phased approach — buy one hearing aid now, save for the second later

A reverse mortgage is best for seniors without steady employment income and who want to age in place without monthly payment obligations.

FAQ

Q: Will a reverse mortgage affect my OAS or GIS? A: No. Reverse mortgage proceeds are classified as loans by the CRA, not income. They don't affect OAS clawback thresholds or GIS calculations. This is a significant advantage over selling your home and investing the proceeds.

Q: Can I still get hearing aids and vision equipment even if I have a reverse mortgage? A: Yes. You can use reverse mortgage funds for any purpose, including sensory health equipment. There are no restrictions on how you spend the money.

Q: What happens if I need a newer hearing aid in five years? A: If you have a reverse mortgage line of credit, you can borrow additional funds for replacement or upgraded equipment. If you have a lump sum, you'd need to plan for future purchases or apply for additional borrowing.

Q: Is there any risk to my home? A: The no-negative-equity guarantee protects you—you can never owe more than your home's market value. However, you must maintain the property, pay property taxes, and keep insurance current (lender requirements).

The Bottom Line

Hearing loss and vision decline are normal parts of aging, but they don't have to limit your independence. Quality sensory equipment helps you stay active, safe, and connected to family and community. For Ontario homeowners 55+, a reverse mortgage can be a smart way to fund these essential purchases without monthly payment stress.

Speak to a licensed mortgage professional. Independent legal advice is required before closing a reverse mortgage in Ontario.

If you're interested in learning more about how a reverse mortgage could support your sensory health needs in retirement, contact Rick Sekhon, a licensed reverse mortgage specialist in Ontario. A free consultation can help you understand your options and determine if this strategy aligns with your goals.

This content is for illustrative purposes only. Rates may vary. Call Rick Sekhon for the best rates and more information.

Ready to Learn More?

Get the free Ontario Reverse Mortgage Guide and find out exactly how much you could unlock from your home.

Get My Free Guide →Related Articles

Reverse Mortgage on a Condo in Ontario: Complete 2026 Guide

Learn about reverse mortgages on condos in Ontario, including eligibility requirements, special considerations, and fees involved.

Read →Working with an Accountant: When Reverse Mortgage Tax Planning Is Worth It

Understand when to hire a CPA for reverse mortgage tax planning. Strategies that save money in retirement income and government benefits.

Read →Protecting Your Home During Separation: Reverse Mortgage Strategy for Spouses

Navigate reverse mortgage implications during spousal separation or divorce in Ontario. Protect equity and understand family law considerations.

Read →